If your credit card application was rejected due to a low credit score or lack of income proof, the fastest fix is a secured (FD-backed) credit card. Deposit ₹2,000–₹5,000, use the card responsibly, repay on time, and your credit score will steadily improve—unlocking better cards later.

How to Build Your Credit Score Fast After Rejection (2026 Guide)

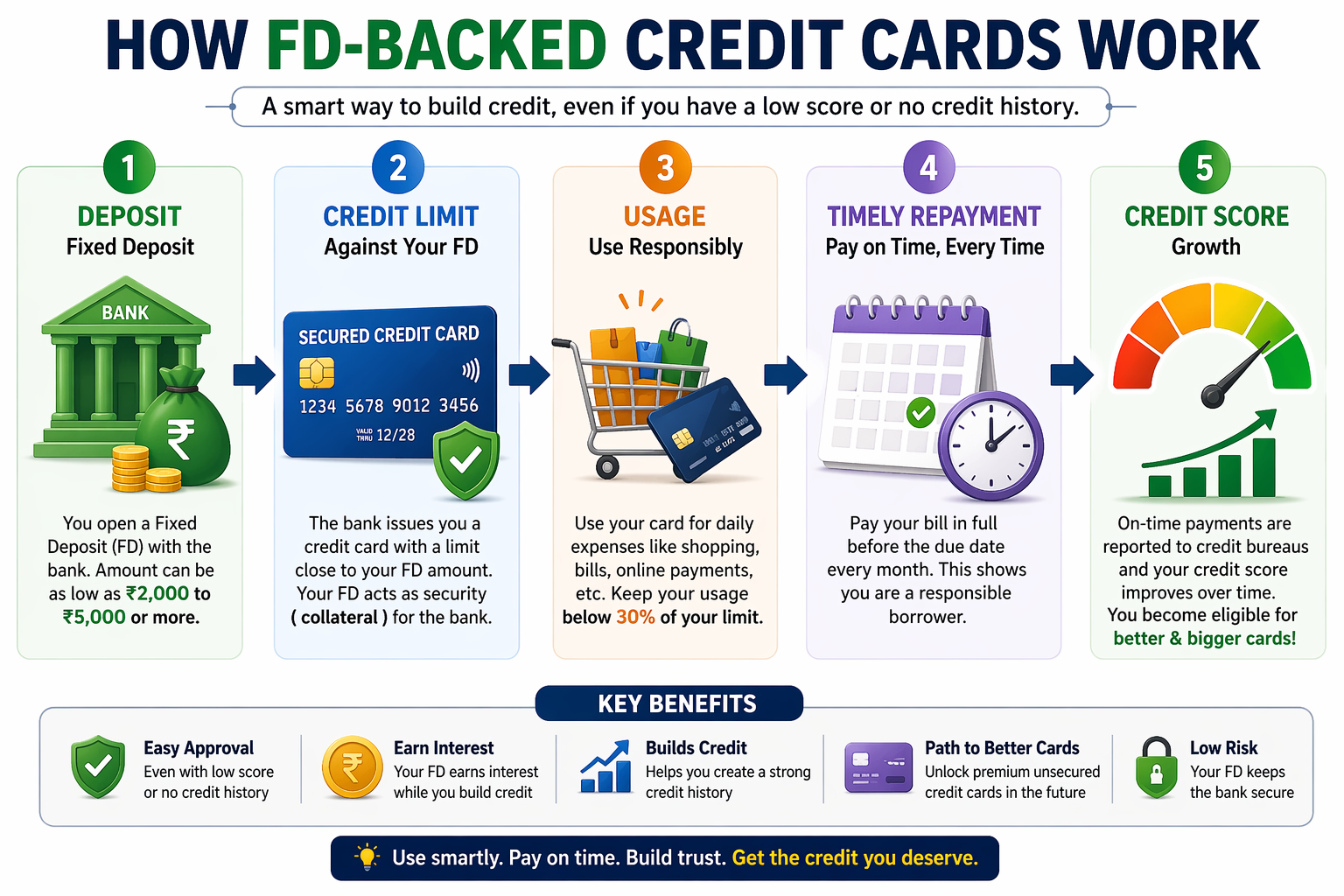

Why was your credit card application rejected—and what actually fixes it?

Most credit card rejections happen for two simple reasons: a low or nonexistent credit score, or missing income proof. I’ve seen this pattern repeatedly—especially among first-time applicants and young professionals. Banks need evidence that you can repay borrowed money, and without a credit history, you’re essentially “invisible” to lenders. That’s where a secured credit card becomes powerful. Instead of relying on your past financial behavior, banks use your fixed deposit (FD) as collateral. This removes their risk and gives you a guaranteed entry point into the credit system. In my experience, this is the most practical workaround in 2026 because it bypasses strict eligibility filters while still helping you build a strong credit profile. Think of it as training wheels for your financial reputation—safe, controlled, and incredibly effective when used correctly.

What is a secured (FD-backed) credit card and how does it work?

A secured credit card—also known as an FD-backed credit card—is issued against a fixed deposit you make with a bank. Typically, you deposit between ₹2,000 and ₹5,000 (or more), and the bank issues a credit limit close to that amount. The key advantage is that your deposit earns interest while simultaneously acting as collateral. I recommend this method because it creates a win-win situation: the bank is protected, and you gain access to credit. You then use this card like any regular credit card—make purchases, pay bills, and most importantly, repay on time. Every on-time payment is reported to credit bureaus, helping you build a positive credit history. Over time, this consistent behavior increases your credit score, making you eligible for unsecured, premium credit cards in the future.

How do you use a secured credit card to build your credit score quickly?

Using a secured credit card effectively is what actually drives results—not just owning one. I always emphasize disciplined usage because that’s what credit bureaus track. Start by using the card for small, regular expenses like groceries or subscriptions. Keep your usage below 30% of your credit limit—this is a critical factor in credit scoring. Next, repay your dues in full and on time every billing cycle. Avoid minimum payments unless absolutely necessary. From what I’ve observed, consistent repayment over 3–6 months can significantly improve your score. Another important step is maintaining continuity—don’t stop using the card after a few months. The longer your positive history, the stronger your profile becomes. This strategy works because it builds trust with lenders, proving that you can manage credit responsibly over time.

Which secured credit cards can you apply for in India?

If you’re starting out, there are a couple of reliable options available right now. Based on what I’ve personally seen and recommended, these two stand out for beginners:

Both cards are designed for users with low or no credit history and offer a straightforward application process. They allow you to open a fixed deposit and instantly get a credit card against it. What makes them useful is their accessibility—you don’t need extensive documentation or a high income to qualify. I suggest comparing features like FD requirements, fees, and app experience before choosing. Either way, both options provide a solid starting point for building your credit profile.

What is the exact step-by-step process to build your credit score?

Here’s the exact system I recommend:

- Open a fixed deposit (₹2,000–₹5,000 or more)

- Apply for a secured credit card against the FD

- Use the card for small, regular expenses

- Keep credit utilization below 30%

- Pay your bill in full before the due date every month

This simple loop—use, repay, repeat—is what steadily builds your credit score. Most users start seeing improvements within a few months.

How does a secured card compare to a regular credit card?

| Feature | Secured Credit Card | Regular Credit Card |

|---|---|---|

| Approval Requirement | Easy (FD required) | Strict (credit score + income) |

| Credit History Needed | Not required | Required |

| Risk to Bank | Low (backed by FD) | High |

| Credit Score Impact | Builds score | Builds or depends on score |

| Ideal For | Beginners / low score users | Experienced users |

Frequently Asked Questions

How long does it take to improve a credit score with a secured card?

Most users see noticeable improvement within 3–6 months if they consistently pay on time and keep utilization low.

Can I withdraw my fixed deposit anytime?

Usually, no. The FD is locked as collateral until you close the credit card. Some banks may allow partial withdrawal under conditions.

Will a secured credit card affect my credit score negatively?

Only if misused. Late payments or high utilization can hurt your score just like a regular credit card.

What happens after my credit score improves?

Once your score improves, you can apply for unsecured credit cards with better rewards and higher limits.

Is ₹2,000 enough to start?

Yes, even a small FD is enough to begin building credit. The key is consistency, not the amount.

Leave a Reply Cancel reply